British Petroleum's Energy Transition Strategy: Challenges in Moving Toward Carbon Neutrality

1. Introduction

The global energy landscape is undergoing one of the most profound transformations in modern history. The accelerating pace of climate change, driven by the persistent rise in greenhouse gas (GHG) emissions, has prompted policymakers, corporations, and civil societies to pursue an urgent shift toward a low-carbon and sustainable energy future. The transition from fossil fuel dependence to renewable and clean energy sources is not merely an environmental necessity but a strategic imperative shaping the long-term competitiveness and survival of global energy corporations. Among these corporations, BP (formerly British Petroleum) has emerged as one of the most visible and ambitious entities undertaking the challenge of energy transition within the oil and gas sector.

Founded in 1909, BP grew to become one of the world’s largest integrated oil and gas companies, with operations spanning exploration, production, refining, distribution, and marketing across more than 70 countries. Historically, BP’s business model was firmly rooted in hydrocarbon extraction and processing, generating significant revenue from crude oil and natural gas. However, over the last two decades, the growing urgency of climate change and the evolving global energy policy environment have forced BP to confront its environmental footprint and reposition itself strategically. The 2010 Deepwater Horizon disaster, which caused massive ecological and reputational damage, marked a turning point in BP’s corporate consciousness, catalyzing a gradual—but determined—shift toward sustainability and transparency.

By 2020, BP announced one of the most ambitious corporate commitments in the global energy industry: to become a “net-zero company by 2050 or sooner.” This commitment encompasses reducing operational (Scope 1 and 2) emissions, cutting carbon intensity of its products (Scope 3 emissions), and investing heavily in renewable energy sources such as wind, solar, hydrogen, and bioenergy. This marked a structural transformation of BP’s identity from an oil and gas company to an integrated energy company. Such a transformation involves not only financial restructuring but also technological innovation, cultural change, and strategic adaptation in response to evolving policy frameworks and stakeholder expectations.

However, this transition is fraught with challenges. The energy sector’s inherent dependency on hydrocarbons, the volatility of renewable markets, fluctuating oil prices, and the complexity of large-scale decarbonization present significant obstacles. Moreover, BP faces the dual challenge of maintaining profitability and shareholder confidence while simultaneously driving long-term sustainability. In this context, BP’s energy transition strategy represents a microcosm of the broader struggle facing the global oil and gas industry—how to achieve carbon neutrality while preserving economic viability.

This study seeks to explore and critically analyze BP’s strategic journey toward carbon neutrality, examining the organizational, financial, technological, and policy-related challenges encountered in this process. It aims to assess how BP aligns its business model, innovation practices, and stakeholder engagement mechanisms with global sustainability imperatives. The research offers insights not only into BP’s internal transformation but also into the wider implications for multinational energy corporations navigating the complex terrain of energy transition.

Research Problem

The research problem centers on understanding how BP can effectively transition from a traditional fossil fuel–based business model to a carbon-neutral organization, given the scale, complexity, and competitive pressures of the global energy industry. Despite public commitments and incremental progress, questions remain about the effectiveness, pace, and authenticity of BP’s transformation.

A key concern lies in the gap between ambition and implementation. While BP has articulated bold climate targets, achieving these goals requires profound structural and operational changes—ranging from technological innovation to investment reallocation and workforce transformation. The company’s financial performance continues to depend heavily on hydrocarbons, creating tension between short-term profitability and long-term sustainability. Furthermore, the global regulatory environment remains fragmented, with inconsistent policy signals across regions, complicating BP’s efforts to design a coherent global strategy.

Another aspect of the research problem involves stakeholder expectations. Investors increasingly demand transparent climate risk disclosures, while governments and consumers expect tangible progress toward renewable energy. Balancing these sometimes conflicting demands requires careful strategic alignment and robust corporate governance. The uncertainty of technological advancement—particularly in areas such as hydrogen energy, carbon capture and storage (CCS), and biofuels adds further complexity.

Thus, the research problem can be framed as follows: How can BP strategically manage the organizational, technological, and financial challenges of transitioning toward carbon neutrality while maintaining global competitiveness and shareholder value? Addressing this question requires a comprehensive understanding of BP’s strategic frameworks, its progress in energy transition initiatives, and the contextual factors influencing its ability to achieve net zero.

Significance

This study holds both academic and practical significance. Academically, it contributes to the growing body of literature on sustainability transitions, corporate environmental strategy, and the strategic management of multinational enterprises in the context of climate change. By focusing on BP,A company with deep historical roots in fossil fuels and a major influence in global energy markets the study offers a valuable case for understanding how legacy corporations navigate transformational change. It builds upon theoretical perspectives from sustainability management, innovation theory, and strategic change management, thereby enhancing understanding of how firms balance economic objectives with environmental imperatives.

Practically, this research offers insights for corporate executives, policymakers, and investors. For corporate leaders, the findings will illuminate effective approaches and pitfalls in managing large-scale sustainability transformations. For policymakers, it provides a case-based understanding of how regulatory and market incentives shape corporate behavior in the energy transition landscape. For investors and stakeholders, it clarifies how corporate commitments translate into measurable action and financial performance.

Moreover, the study’s focus on BP’s global operations offers lessons for international strategy formulation in the era of decarbonization. As the global economy transitions toward renewable energy, understanding BP’s strategic adaptation provides a framework for assessing the feasibility and scalability of net-zero ambitions across industries. Ultimately, the study contributes to global discourse on sustainable business transformation and corporate accountability in addressing climate change.

2. LITERATURE REVIEW

2.1 The Concept of Energy Transition and Global Decarbonization

The concept of energy transition represents a fundamental transformation in the way societies produce, distribute, and consume energy. It is a multidimensional process driven by environmental, technological, economic, and policy factors, primarily aimed at reducing greenhouse gas (GHG) emissions and mitigating climate change. According to Sovacool (2016), energy transitions are not merely technological shifts but complex socio-technical processes that reshape economic systems, governance models, and corporate strategies. The current global energy transition from fossil fuel dependence to low-carbon and renewable energy systems—is arguably the most far-reaching industrial transformation since the First Industrial Revolution.

At the heart of this transition lies the concept of decarbonization, which involves the systematic reduction of carbon dioxide (CO₂) and other GHG emissions from energy systems. The Paris Agreement of 2015, adopted under the United Nations Framework Convention on Climate Change (UNFCCC), catalyzed global efforts to achieve net-zero emissions by mid-century, prompting corporations and governments to redefine their energy portfolios. IEA (2022) notes that achieving net-zero by 2050 would require a 90% reduction in carbon emissions from power generation, transport, and heavy industries. This macro-level shift has profound implications for traditional oil and gas companies such as BP, Shell, ExxonMobil, and Total Energies, whose historical core competencies are rooted in fossil energy extraction and refining.

The energy transition can be interpreted through the lens of systems transition theory, which describes how incumbent systems evolve through innovation, niche experimentation, and structural change (Geels, 2002). Within this framework, the fossil fuel-based energy regime is being disrupted by renewable energy technologies such as wind, solar, hydrogen, and advanced biofuels. The gradual scaling of these innovations combined with regulatory pressure and stakeholder activism—is eroding the dominance of carbon-intensive systems. For companies like BP, this means not only investing in clean energy but also reconfiguring their organizational architecture, value propositions, and stakeholder engagement strategies to remain competitive in a carbon-constrained world.

From a strategic management perspective, energy transition demands firms to exercise dynamic capabilities the ability to sense environmental changes, seize emerging opportunities, and transform internal processes (Teece, Pisano & Shuen, 1997). BP’s transition strategy, unveiled in 2020, exemplifies this approach by announcing a shift from an International Oil Company (IOC) to an Integrated Energy Company (IEC). This shift reflects a recognition that long-term competitiveness now depends on flexibility, innovation, and cross-sectoral integration. BP’s investments in offshore wind, electric vehicle charging networks, and hydrogen hubs are part of a broader attempt to reposition itself within the evolving global energy ecosystem.

At the same time, the energy transition presents institutional and governance challenges. Regulatory frameworks such as the European Union’s Green Deal and the United Kingdom’s Net Zero Strategy are accelerating the pace of decarbonization while imposing new compliance costs on corporations. Meadowcroft (2011) argues that effective governance in transitions requires coordination between public and private actors, as no single entity can drive systemic change alone. For global energy corporations, this creates a dual challenge: aligning with regulatory and societal expectations while ensuring profitability in volatile markets.

The economic dimension of the energy transition is equally critical. Fossil fuels still account for about 80% of global primary energy consumption (BP Statistical Review, 2023). Yet, the cost of renewable technologies has declined dramatically solar power costs have fallen by over 85% since 2010 (IRENA, 2022). These trends create both threats and opportunities. Companies heavily invested in hydrocarbons face the risk of asset stranding, where fossil reserves may become unexploitable due to climate regulations. Conversely, early movers in renewables can capture new growth markets. For BP, the economic rationale for transition lies in diversifying its energy portfolio to hedge against oil price volatility while tapping into expanding clean energy sectors.

Furthermore, social and ethical pressures are reshaping the energy landscape. Stakeholders—including investors, governments, consumers, and civil society organizations—are demanding greater transparency and accountability regarding environmental impacts. Frameworks such as Environmental, Social, and Governance (ESG) reporting and the Task Force on Climate-related Financial Disclosures (TCFD) are institutionalizing sustainability metrics in corporate decision-making. According to Freeman’s (1984) Stakeholder Theory, firms must create value not only for shareholders but also for employees, customers, and society at large. BP’s energy transition efforts, therefore, must be understood as both a strategic and ethical response to evolving stakeholder expectations.

From a technological innovation standpoint, the transition is being fueled by advancements in digitalization, smart grids, and storage technologies. The integration of artificial intelligence, data analytics, and Internet of Things (IoT) applications is enabling greater efficiency and flexibility in energy systems (Schot & Geels, 2008). BP’s digital transformation initiatives such as predictive maintenance in upstream operations and AI-driven energy management platforms illustrate how technology serves as an enabler of decarbonization.

Finally, the global geopolitical dimension cannot be ignored. The Russia–Ukraine conflict of 2022 underscored the strategic vulnerabilities of fossil fuel dependency, prompting Europe and other regions to accelerate renewable adoption. At the same time, emerging economies such as China and India are investing heavily in renewables while still relying on coal to sustain economic growth. This asymmetrical energy landscape complicates global coordination, as countries pursue diverse pathways toward carbon neutrality. For multinational energy firms like BP, operating across these divergent markets requires balancing local adaptation with global coherence a theme that runs through this entire dissertation.

2.2 Theoretical Perspectives on Corporate Sustainability and Strategic Change

Corporate sustainability has evolved from a peripheral concern into a central component of strategic management and corporate governance. In the context of the global energy transition, it represents both an ethical commitment and a competitive imperative. The theoretical foundations that underpin corporate sustainability and strategic change in multinational corporations such as BP can be traced to several overlapping schools of thought including the Resource-Based View (RBV), Dynamic Capabilities Theory, Stakeholder Theory, and Institutional Theory each offering distinct insights into how firms internalize environmental challenges and transform them into strategic opportunities.

The Resource-Based View (RBV) and Sustainable Competitive Advantage

The Resource-Based View, developed by Wernerfelt (1984) and expanded by Barney (1991), posits that sustainable competitive advantage arises from the possession and deployment of valuable, rare, inimitable, and non-substitutable (VRIN) resources. In the energy sector, traditional sources of advantage — such as control over hydrocarbon reserves, refining capacity, and distribution networks are increasingly being challenged by technological innovation, regulatory change, and societal expectations for decarbonization. As Hart (1995) argues in his “Natural-Resource-Based View (NRBV),” a firm’s capability to reduce pollution, design environmentally benign products, and adopt sustainable technologies can itself become a strategic asset.

For BP, the transition to a low-carbon business model entails reconfiguring its resource base: human capital in renewable engineering, technological assets in wind and solar power, and intangible assets such as brand reputation and stakeholder trust. These elements, when integrated, form the foundation of a new competitive advantage aligned with sustainability imperatives. BP’s strategic investments in offshore wind partnerships (e.g., with Equinor in the U.S.) and green hydrogen initiatives exemplify how the NRBV framework can guide traditional energy firms toward innovation-led sustainability.

Dynamic Capabilities and Strategic Renewal

While the RBV emphasizes the possession of strategic resources, the Dynamic Capabilities Framework focuses on a firm’s ability to adapt, integrate, and reconfigure those resources in response to environmental change (Teece, Pisano & Shuen, 1997). Energy transition represents a high-velocity context where technological, regulatory, and social dynamics evolve rapidly. Firms that succeed are those capable of continuously sensing market shifts, seizing emerging opportunities, and transforming their organizational architecture to sustain growth.

BP’s reorganization under CEO Bernard Looney in 2020 reflects a manifestation of dynamic capabilities in action. The company redefined its mission “Reimagining Energy for People and Our Planet” — and committed to reducing its oil and gas production by 40% by 2030 while expanding investments in renewables and convenience businesses. These moves illustrate the processes of strategic sensing (identifying low-carbon trends), seizing (investing in renewable ventures), and transforming (restructuring internal operations), all of which are core components of dynamic capability deployment.

However, scholars such as Eisenhardt and Martin (2000) caution that dynamic capabilities are not universally effective; they must be context-specific and embedded within appropriate organizational routines. For BP, this means aligning internal governance structures, talent development, and knowledge-sharing systems with its new sustainability-driven strategy. The establishment of integrated business groups — such as gas and low carbon energy, customers and products, and innovation & engineering exemplifies this structural reconfiguration designed to institutionalize change.

Stakeholder Theory and Corporate Legitimacy

Freeman’s (1984) Stakeholder Theory provides another vital perspective, asserting that corporations exist within a network of relationships involving employees, customers, investors, regulators, and communities. Long-term success depends on creating value for all stakeholders, not merely shareholders. In the energy industry, where environmental externalities are significant, stakeholder engagement becomes a crucial determinant of corporate legitimacy.

BP’s sustainability strategy explicitly integrates stakeholder perspectives through initiatives like its Sustainability Framework, which outlines goals related to emissions reduction, people and planet, and social inclusion. Moreover, BP’s participation in collaborative industry platforms such as the Oil and Gas Climate Initiative (OGCI) highlights its effort to maintain legitimacy through collective action. According to Donaldson and Preston (1995), legitimacy and moral obligation are intrinsic to stakeholder management, which enhances a firm’s reputation and long-term viability.

Nevertheless, BP’s history including incidents such as the Deepwater Horizon oil spill in 2010 demonstrates the fragility of stakeholder trust and the reputational risks inherent in sustainability transitions. Post-crisis, the company’s attempts to rebuild trust through transparent ESG reporting and public commitments to net-zero are consistent with the institutional isomorphism described by DiMaggio and Powell (1983), where firms adopt socially acceptable practices to conform to external norms and regain legitimacy.

Institutional Theory and Strategic Change

Institutional theory emphasizes the influence of societal norms, regulations, and cultural expectations on organizational behavior (Scott, 2008). In the global energy context, institutional pressures come from multiple levels supranational (e.g., Paris Agreement, IPCC guidelines), national (e.g., UK’s Climate Change Act), and industry-level (e.g., ESG disclosure standards). BP’s transition cannot be viewed purely as a voluntary strategic shift; it is also a response to coercive (regulatory), normative (professional and societal), and mimetic (competitive) pressures that shape the behavior of multinational corporations.

The concept of institutional entrepreneurship (Greenwood & Suddaby, 2006) is particularly relevant here. It refers to organizations that leverage their resources and influence to reshape institutional environments. BP, through its active engagement in policy dialogue and partnerships with renewable startups, can be seen as both a subject and an agent of institutional change. By publicly aligning with the 1.5°C climate target and setting science-based emission reduction goals, BP contributes to the diffusion of new norms that redefine success in the energy sector.

Triple Bottom Line and Sustainable Value Creation

Elkington’s (1997) Triple Bottom Line (TBL) framework extends the notion of performance beyond financial outcomes to include social and environmental dimensions — “People, Planet, and Profit.” This multidimensional view aligns closely with modern conceptions of corporate purpose and sustainability reporting. BP’s annual sustainability reports increasingly adopt the TBL logic by emphasizing decarbonization targets, social equity initiatives, and economic resilience.

Integrating the TBL perspective into strategy requires balancing trade-offs between short-term profitability and long-term environmental stewardship. For instance, while divesting from fossil assets may reduce near-term revenues, it enhances corporate resilience against future regulatory risks and strengthens brand equity among socially responsible investors. Porter and Kramer’s (2011) concept of Creating Shared Value (CSV) further supports this by asserting that corporate success and societal progress are mutually reinforcing. BP’s investment in clean energy technologies thus represents both a moral and strategic pursuit aligning economic imperatives with environmental and social outcomes.

Strategic Change and Organizational Learning

Energy transition is not a static goal but a continuous process of organizational learning and adaptation. Argyris and Schön (1978) describe “double-loop learning,” where organizations question and revise their underlying assumptions and strategies, not just operational routines. For BP, this involves rethinking what “energy” means, how it is delivered, and how success is measured. The firm’s pivot toward customer-centric and service-oriented business models (e.g., EV charging, digital energy management) signals a deep learning process that transcends incremental change.

Strategic change literature also highlights the importance of leadership and vision in driving transformation (Kotter, 1996). BP’s leadership, particularly under Looney, has articulated a clear narrative linking sustainability to corporate purpose “Performing while Transforming.” Such vision provides direction, mobilizes internal commitment, and signals credibility to external stakeholders. Yet, as Burnes (2017) emphasizes, sustaining change requires alignment between structure, culture, and strategy an ongoing challenge for legacy energy companies undertaking radical transformation.

Integration of Theoretical Perspectives

Taken together, these theoretical frameworks offer a multidimensional understanding of how corporations like BP navigate sustainability transitions. The RBV and dynamic capabilities explain how firms leverage internal assets and competencies to innovate; stakeholder and institutional theories illuminate how external pressures shape legitimacy and strategic direction; and TBL and learning theories emphasize the integration of environmental and social considerations into long-term performance models.

This synthesis provides the conceptual foundation for analyzing BP’s transition strategy as a process of aligning internal resources with external expectations, transforming organizational identity, and constructing a new form of sustainable competitiveness in a carbon-constrained world.

2.3 Global Climate Policies and Carbon Neutrality Targets

The global movement toward decarbonization is fundamentally rooted in international climate policy frameworks that have evolved over the past three decades. These frameworks establish both normative and regulatory foundations for national governments and corporations to pursue carbon neutrality, creating a structured environment in which firms such as BP must operate and strategically adapt. Global climate policies have progressively shifted from voluntary environmental stewardship to binding commitments and measurable outcomes, reflecting the growing urgency of mitigating anthropogenic climate change.

The Evolution of Global Climate Governance

The institutionalization of climate governance began with the United Nations Framework Convention on Climate Change (UNFCCC) in 1992, which established the principle of “common but differentiated responsibilities.” This principle recognized that while all nations share the obligation to address climate change, developed countries bear greater responsibility due to their historical emissions. The Kyoto Protocol (1997) marked the first legally binding international agreement requiring industrialized countries to reduce greenhouse gas (GHG) emissions relative to 1990 levels. However, its limited participation and lack of enforcement mechanisms restricted its effectiveness (Victor, 2011).

The turning point came with the Paris Agreement (2015), which introduced a universal framework for action. Its central objective — to limit global temperature rise to “well below 2°C above pre-industrial levels” and pursue efforts to limit it to 1.5°C — fundamentally reshaped international energy and environmental policy. Unlike Kyoto, the Paris Agreement adopted a bottom-up structure based on Nationally Determined Contributions (NDCs), allowing each country to set its own emission reduction targets. This flexibility enhanced participation but also placed greater emphasis on domestic implementation and private-sector engagement.

Under the Paris framework, corporations became integral actors in achieving climate goals. Governments increasingly rely on market-based instruments, such as carbon pricing, emissions trading schemes (ETS), and renewable energy certificates, to drive corporate behavior. According to Rogelj et al. (2018), achieving net-zero by 2050 requires transformative shifts in energy production, industrial systems, and consumption patterns effectively redefining the boundaries of corporate strategy in carbon-intensive sectors.

Regional and National Carbon Neutrality Commitments

The global policy landscape is characterized by regional heterogeneity. The European Union (EU) has emerged as a leader through its European Green Deal, adopted in 2019, which legally commits member states to achieving net-zero emissions by 2050. The EU Emissions Trading System (EU ETS), the world’s largest carbon market, serves as the cornerstone of this policy. By establishing a cap-and-trade mechanism, it incentivizes companies to internalize the cost of carbon emissions. For multinational corporations like BP, compliance with EU ETS requirements directly influences operational costs, investment decisions, and portfolio diversification.

The United Kingdom’s Climate Change Act (2008) — the first national law to establish legally binding carbon budgets — further underscores the tightening policy environment. Following its withdrawal from the EU, the UK reaffirmed its climate leadership by enacting a target of net-zero by 2050, enforced through the Climate Change Committee (CCC). For BP, headquartered in London, these national commitments serve as both constraints and opportunities. Compliance pressures push the company to accelerate its decarbonization pathway, while supportive policy instruments (such as offshore wind subsidies and hydrogen innovation grants) open new avenues for growth.

Globally, China’s commitment to carbon neutrality by 2060 and the United States’ re-entry into the Paris Agreement in 2021 have created a new wave of momentum. The convergence of policy objectives across major economies signals a structural transformation in global energy systems. According to IEA (2022), over 140 countries now have net-zero pledges covering more than 90% of global GDP and emissions. This policy harmonization is gradually reducing the “first-mover disadvantage” for companies transitioning early, creating a more level competitive playing field for decarbonization investment.

Market-Based Mechanisms and Corporate Adaptation

A key feature of contemporary climate policy is the reliance on market-based instruments to drive emissions reduction. Stavins (2021) explains that such mechanisms create price signals that reward low-carbon innovation and penalize carbon intensity. For instance, carbon pricing — through taxes or trading systems — compels firms to internalize environmental externalities. As a result, carbon-intensive business models face erosion of profitability, while firms with cleaner energy portfolios gain relative advantage.

BP’s adaptation strategy reflects this shift. The company has begun integrating internal carbon pricing into its investment appraisal processes to reflect future policy risks. By anticipating regulatory costs, BP can better allocate capital toward low-carbon ventures such as solar, wind, and bioenergy. Additionally, the company supports the expansion of global carbon markets, viewing them as instruments to stimulate investment in scalable, cost-effective decarbonization technologies.

Moreover, corporate engagement in voluntary carbon offset programs and Science-Based Targets initiatives (SBTi) further illustrates how private actors operationalize policy objectives. BP’s commitment to align its emission trajectory with a 1.5°C pathway represents not just compliance but strategic foresight. Through participation in global alliances such as the Task Force on Climate-related Financial Disclosures (TCFD), BP enhances transparency and signals accountability to investors — a practice aligned with the growing importance of Environmental, Social, and Governance (ESG) standards in financial markets (Kotsantonis, Pinney & Serafeim, 2016).

Policy-Induced Innovation and the Transition to Low-Carbon Energy

Climate policies also function as drivers of innovation. Porter and van der Linde (1995) introduced the “Porter Hypothesis,” arguing that well-designed environmental regulations can stimulate technological innovation that enhances both environmental performance and competitiveness. This view challenges the traditional notion that sustainability undermines profitability, instead framing regulation as a catalyst for modernization.

BP’s response to such regulatory dynamics illustrates this mechanism in practice. The company’s increasing R&D expenditure on renewable energy systems, its investment in low-carbon start-ups through BP Ventures, and its strategic partnerships with governments and technology firms demonstrate a proactive approach to innovation under policy pressure. For example, BP’s participation in the UK’s North Sea Transition Deal aims to combine government incentives with corporate investment to develop carbon capture and storage (CCS) and hydrogen technologies.

Furthermore, policy frameworks like the EU Taxonomy for Sustainable Activities and the Corporate Sustainability Reporting Directive (CSRD) are reshaping capital allocation by defining what constitutes sustainable investment. Institutional investors, influenced by these regulations, are directing funds toward companies with clear decarbonization pathways. For BP, aligning its strategy with these criteria enhances access to green financing and reinforces investor confidence.

Challenges of Global Policy Coordination

Despite widespread commitments to carbon neutrality, achieving coordinated global action remains a complex challenge. Differing national interests, economic dependencies, and development priorities create asymmetries in implementation. Keohane and Victor (2016) argue that the global climate regime operates as a “regime complex” — a decentralized system of overlapping and sometimes competing institutions. This fragmentation complicates corporate planning for multinational firms like BP, which operate across jurisdictions with varying carbon prices, regulatory timelines, and reporting standards.

Moreover, carbon leakage the relocation of emissions-intensive activities to regions with weaker regulations — poses a persistent risk. To mitigate this, the EU has proposed the Carbon Border Adjustment Mechanism (CBAM), designed to equalize carbon costs for imports and domestic production. Such instruments will directly affect energy exporters and multinational producers, reinforcing the global diffusion of carbon accountability.

Corporate Climate Commitments and Policy Alignment

In response to global and regional policies, corporations have increasingly adopted science-based emission targets and net-zero pledges. However, scholars such as Anderson and Peters (2016) caution that many corporate commitments rely heavily on offsetting rather than absolute emission reductions, raising concerns about credibility and transparency. BP’s commitment to achieve net-zero across its operations by 2050, coupled with its aim to reduce operational emissions by 30–35% by 2030, demonstrates a relatively robust approach yet its continued involvement in oil and gas exploration underscores the inherent tension between transition and continuity.

The alignment between corporate and policy objectives thus becomes a measure of strategic coherence. Bansal and Roth (2000) argue that firms engaging in genuine sustainability transformation exhibit a proactive posture, integrating environmental goals into their strategic core, rather than treating them as compliance obligations. BP’s decision to embed sustainability metrics into executive remuneration and corporate governance reflects this integration, translating external policy pressures into internal performance incentives.

2.4 The Role of Oil and Gas Majors in the Energy Transition

The global shift toward low-carbon energy systems represents one of the most profound transformations in modern industrial history. Within this context, oil and gas majors—including BP, Shell, TotalEnergies, ExxonMobil, and Chevron—stand at the intersection of economic necessity, political pressure, and technological opportunity. These corporations, often referred to as “supermajors,” have historically shaped global energy markets, controlled vast reserves, and influenced geopolitical dynamics. As the world accelerates toward decarbonization, these same entities now face existential questions about their role, relevance, and adaptability in a carbon-constrained future.

The energy transition challenges the core logic of these companies’ business models, which for over a century have been anchored in hydrocarbon exploration, production, and refining. Unlike firms in other sectors that can decarbonize primarily through process efficiency or renewable energy procurement, oil majors must undertake structural reinvention—transforming not only how they produce energy, but what kind of energy they produce. This requires reconfiguring technological capabilities, capital allocation, and corporate culture on a global scale (Steffen et al., 2018).

2.4.1 Historical Dependence and the Path to Transformation

The historical development of the oil industry has been synonymous with industrialization, globalization, and economic growth. For decades, the profitability of oil majors was secured through the “resource-rent model”, whereby access to hydrocarbon reserves generated long-term economic returns insulated from short-term volatility. This model, however, is increasingly untenable in the face of climate constraints, investor activism, and societal expectations.

Since the 2010s, growing alignment between climate science, policy, and finance has altered the strategic calculus of fossil fuel firms. The Intergovernmental Panel on Climate Change (IPCC) reports have consistently highlighted the need for rapid decarbonization to limit global warming to 1.5°C, implying that a significant share of proven oil reserves must remain unburned,a phenomenon termed “stranded assets” (Carbon Tracker Initiative, 2013). Consequently, the traditional growth strategies of oil majors are under increasing scrutiny from regulators and shareholders alike.BP’s evolution illustrates this paradigm shift. Historically branded as “Beyond Petroleum” during its early 2000s sustainability rebranding, BP was among the first oil majors to publicly acknowledge climate change as a core strategic issue. However, after the Deepwater Horizon disaster (2010), the company temporarily retreated from renewable investments to restore its balance sheet. Its renewed commitment to net-zero in 2020 marked a second-generation transformation, reflecting lessons learned from both operational crises and shifting global expectations.

2.4.2 Strategic Reorientation: From Hydrocarbon Dependency to Integrated Energy Firms

The ongoing energy transition has prompted oil and gas majors to adopt diversification strategies that reposition them as integrated energy companies rather than pure hydrocarbon producers. BP’s strategic framework, articulated in its “Reimagining Energy” plan (2020), exemplifies this approach. The company aims to reduce oil and gas production by 40% by 2030, increase annual low-carbon investment to $5 billion, and expand renewable capacity to 50 gigawatts (GW).

This mirrors broader industry trends. Shell has invested heavily in electric mobility, hydrogen, and biofuels, while TotalEnergies rebranded itself to reflect a cross-energy portfolio integrating gas, renewables, and electricity. In contrast, ExxonMobil and Chevron have pursued more conservative pathways, focusing on emissions reduction within traditional operations rather than systemic diversification. These differences reveal a strategic spectrum within the industry, ranging from transition leadership (BP, TotalEnergies) to defensive adaptation (ExxonMobil).From a theoretical standpoint, such transformations align with the Dynamic Capabilities Framework (Teece, 2007), which emphasizes the need for firms to sense environmental shifts, seize opportunities, and reconfigure resources accordingly. BP’s early investments in solar, offshore wind, and electric vehicle (EV) charging infrastructure demonstrate an attempt to deploy dynamic capabilities across emerging low-carbon markets. By leveraging its global infrastructure, technical expertise, and capital strength, BP seeks to position itself not merely as a reactor to policy but as a proactive architect of the energy transition.

2.4.3 Technological Innovation and R&D Reorientation

Innovation remains the cornerstone of the transition from fossil-based energy systems to renewable and hybrid models. For oil majors, this involves a reallocation of R&D resources from traditional petroleum engineering toward clean technologies such as carbon capture, utilization, and storage (CCUS), hydrogen, and advanced biofuels.

BP’s R&D strategy has evolved significantly. The company operates multiple innovation hubs, including the BP Ventures and Launchpad divisions, which invest in climate-tech start-ups focusing on energy storage, AI-driven grid optimization, and decarbonized mobility. Its partnership with Lightsource BP,a solar developer with projects in over 15 countries represents a major diversification of its R&D ecosystem. Through these ventures, BP integrates external knowledge and entrepreneurial agility with its internal engineering capabilities, consistent with the principles of open innovation (Chesbrough, 2003).

Similarly, TotalEnergies and Shell have established dedicated innovation clusters to explore synthetic fuels and green hydrogen, while ExxonMobil invests heavily in CCUS through its Low Carbon Solutions division. However, critics argue that despite increased R&D expenditure, the ratio of low-carbon investment to total capital spending remains disproportionately low typically below 10% for most majors (IEA, 2023). This gap underscores the tension between short-term shareholder returns and long-term sustainability imperatives.

2.4.4 Financial Market Pressure and ESG Accountability

One of the most significant drivers of transformation has been the financialization of climate risk. Investors, asset managers, and sovereign funds are increasingly integrating Environmental, Social, and Governance (ESG) metrics into portfolio decisions, pressuring fossil fuel companies to align with sustainability standards. For example, in 2021, shareholders forced ExxonMobil to appoint climate-conscious board members through activist investor group Engine No. 1, signaling a shift in investor expectations across the sector.

BP’s strategic repositioning has also been shaped by investor sentiment. The company’s commitment to reduce operational emissions by 35–40% by 2030 and to achieve net-zero across operations by 2050 aligns with the expectations of institutions adhering to the UN Principles for Responsible Investment (PRI). Moreover, BP’s issuance of green bonds and transparent reporting through the Task Force on Climate-related Financial Disclosures (TCFD) demonstrate growing alignment between financial governance and sustainability.

However, the transition entails trade-offs. Divestment from oil assets and reduced hydrocarbon output can erode short-term profitability, leading to market skepticism and share price volatility. The challenge lies in reconciling investor confidence with transformation costs a dilemma that defines the contemporary strategic landscape of oil majors.

2.4.5 Policy and Geopolitical Dependencies

The strategic direction of oil majors is deeply influenced by global energy policy, geopolitical realities, and market regulation. Access to fossil fuel reserves remains entwined with geopolitical considerations, as exemplified by tensions in the Middle East and Russia’s role in global energy supply. The Ukraine conflict (2022) further accelerated European efforts to reduce dependency on Russian hydrocarbons, thereby intensifying the push for renewable energy self-sufficiency.

BP’s withdrawal from Rosneft, Russia’s state-controlled oil company, in 2022—at an estimated $25 billion loss—highlights the vulnerability of multinational energy firms to geopolitical risk. Yet it also reinforced BP’s alignment with ethical and sustainability imperatives consistent with Western decarbonization agendas. In contrast, ExxonMobil and Chevron’s operations in politically volatile regions demonstrate that transition strategies are context-dependent, shaped by differing national energy policies, market incentives, and stakeholder expectations.

Moreover, the carbon border adjustment mechanisms (CBAM) proposed by the European Union and similar policies elsewhere are poised to penalize carbon-intensive imports, further pressuring oil exporters and multinational producers. Thus, policy alignment is not merely a compliance issue but a strategic determinant of competitiveness.

2.4.7 Collaborative Ecosystems and Public-Private Partnerships

Oil and gas majors increasingly recognize that achieving carbon neutrality cannot be accomplished in isolation. As Geels (2014) suggests, energy transitions are “socio-technical transformations” involving networks of governments, industries, and civil society. Accordingly, collaboration through public-private partnerships (PPPs), industry coalitions, and research alliances has become essential.

BP’s partnerships with entities like Equinor, Microsoft, and Ørsted illustrate this collaborative model. The company’s co-investment in offshore wind farms, digital energy management platforms, and carbon capture infrastructure demonstrates a networked approach to innovation. These alliances not only distribute risk but also accelerate technological learning and standardization.

Moreover, initiatives such as the Oil and Gas Climate Initiative (OGCI),a CEO-led consortium of 12 major companies including BP, Shell, and TotalEnergies,serve as industry-level mechanisms for sharing best practices and financing low-carbon technologies. While critics question their efficacy, such platforms signal a shift toward collective accountability in global energy governance.

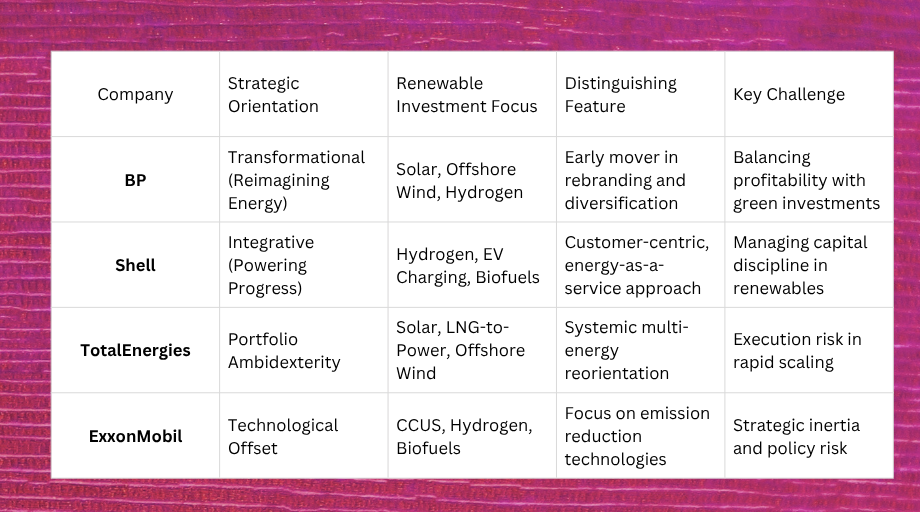

2.5 Comparative Review of Energy Transition Strategies (Shell, TotalEnergies, ExxonMobil)

The global energy transition has compelled all major oil and gas corporations to reconsider their traditional business models. While they share common exposure to climate policy risks, investor activism, and technological disruption, their strategic responses vary significantly. This divergence reflects differences in corporate governance, national regulation, risk appetite, and cultural orientation. A comparative review of Shell, TotalEnergies, and ExxonMobil three of the most influential oil majors alongside BP provides valuable insight into the strategic heterogeneity of the industry’s decarbonization efforts.

From a theoretical standpoint, this analysis aligns with the Strategic Choice Theory (Child, 1972), which posits that organizations retain agency in determining how they adapt to environmental changes. Even under identical macro pressures, firms interpret and act upon signals differently depending on their internal values, leadership, and resource base. Applying this lens, BP, Shell, and TotalEnergies exhibit proactive transition behaviors, whereas ExxonMobil represents a reactive adaptation model, reflecting a more conservative corporate ideology.

2.5.1 Shell: “Powering Progress” through Integrated Energy Systems

Shell’s transition strategy formalized under the framework “Powering Progress” in 2021 positions the company as a fully integrated energy solutions provider. Its ambition to become a net-zero emissions energy business by 2050 encompasses not only operational emissions (Scope 1 and 2) but also customer emissions (Scope 3), demonstrating a more holistic approach than many of its peers.

Shell’s global energy portfolio includes liquefied natural gas (LNG), renewable power generation, hydrogen infrastructure, and carbon offset programs. A cornerstone of its strategy lies in the expansion of electric vehicle (EV) charging networks, with Shell operating more than 50,000 charging points globally and targeting over 500,000 by 2030. This reflects a shift from commodity-based operations toward customer-centric, service-driven energy ecosystems.From a resource-based view (RBV) perspective (Barney, 1991), Shell’s core competencies in logistics, technology integration, and large-scale project management are being redeployed in renewable domains. Its acquisitions of Sonnen (battery storage), Ubitricity (EV charging), and Savion (solar power) indicate a deliberate pursuit of complementary capabilities that reinforce its new energy identity.

Nevertheless, Shell’s strategy has faced challenges, particularly in reconciling shareholder returns with capital-intensive renewables. In 2023, CEO Wael Sawan announced a recalibration of investment priorities, signaling a partial return to high-margin LNG and deepwater projects. This move underscores the ongoing tension between short-term profitability and long-term sustainability—a tension inherent to the energy transition for all major oil companies.

2.5.2 TotalEnergies: A Systemic Transformation Anchored in Rebranding

Among all oil majors, TotalEnergies arguably represents the most structurally comprehensive reorientation toward a low-carbon identity. Its 2021 rebranding from Total SA to TotalEnergies SE symbolized a conscious break from its fossil-centric legacy. CEO Patrick Pouyanné articulated the company’s vision as becoming a “multi-energy company” that delivers oil, natural gas, electricity, hydrogen, biomass, and renewables within a unified business framework.TotalEnergies’ transition strategy emphasizes portfolio balance. The company targets 50% of its energy mix from gas, 25% from renewables and electricity, and 25% from liquids by 2050. It plans to install 100 GW of renewable capacity by 2030—double BP’s current target—and operates large-scale projects in solar, offshore wind, and battery storage across Europe, Asia, and Africa.

The company’s investment discipline differentiates it from many peers. TotalEnergies maintains profitability in oil operations while using these earnings to fund renewable expansion—a strategy consistent with the ambidexterity theory (O’Reilly & Tushman, 2013), which posits that firms must exploit existing capabilities while exploring new opportunities. Its integration of renewables with downstream gas operations, especially through liquefied natural gas-to-power projects, demonstrates a pragmatic transition model rather than an abrupt transformation.From a governance standpoint, Total Energies embeds sustainability into its board structure through a dedicated Sustainability & Climate Committee, aligning executive compensation with carbon intensity reduction targets. The company’s transparency in climate reporting under the Task Force on Climate-related Financial Disclosures (TCFD) and alignment with the Science Based Targets initiative (SBTi) reflect a deeper institutionalization of ESG accountability than many competitors.

However, the company’s aggressive renewables expansion raises questions about execution risk. Integrating diverse energy assets, managing geopolitical exposure, and sustaining shareholder returns amid market volatility remain formidable challenges. Nonetheless, TotalEnergies’ transformation exemplifies how strategic clarity and financial prudence can coexist within the broader decarbonization agenda.

2.5.3 ExxonMobil: Defensive Adaptation and Carbon Capture Leadership

In contrast to its European peers, ExxonMobil has adopted a conservative and defensive stance in the energy transition. Historically, ExxonMobil has prioritized shareholder value through disciplined capital allocation in hydrocarbons, resisting what it perceives as premature or unprofitable diversification into renewables. Until recently, the company’s corporate narrative emphasized emission reduction through technology, rather than systemic portfolio transformation.

The establishment of ExxonMobil Low Carbon Solutions in 2021 marked a subtle but significant strategic shift. The division focuses on carbon capture, utilization, and storage (CCUS), hydrogen production, and biofuels—technologies aligned with ExxonMobil’s existing competencies in large-scale engineering and process optimization. The company plans to invest approximately $17 billion in lower-emission initiatives through 2027, reflecting a measured approach to transition investments (ExxonMobil Annual Report, 2023).From a theoretical perspective, ExxonMobil’s strategy corresponds to the Path Dependence Theory (David, 1985), which explains how historical investments and organizational routines constrain strategic flexibility. The company’s technological strengths in petrochemicals and refining create high switching costs, discouraging rapid diversification. Moreover, its U.S. domicile subjects it to less stringent climate regulation compared to European counterparts, reinforcing its hydrocarbon orientation.Critics argue that ExxonMobil’s emphasis on CCUS represents a technological offset strategy rather than genuine decarbonization. While CCUS can play a crucial role in hard-to-abate sectors, its scalability and economic viability remain uncertain. Nonetheless, ExxonMobil’s expertise in subsurface engineering positions it as a potential leader if CCUS technology achieves widespread deployment.

The firm’s limited engagement in renewable power generation contrasts sharply with BP and TotalEnergies. Yet, ExxonMobil’s strategic conservatism may yield resilience in the short term, particularly amid volatile oil markets. The company’s high return on capital employed (ROCE) and low debt ratio ensure robust financial health, offering flexibility to pivot when renewable technologies achieve higher maturity and profitability.

2.5.4 Comparative Strategic Analysis: BP, Shell, TotalEnergies, ExxonMobil

A comparative lens reveals both convergence and divergence among oil majors in navigating the energy transition. The convergence lies in their shared recognition of the inevitability of decarbonization, investor pressure, and technological disruption. Divergence, however, emerges in the depth, speed, and scope of their strategic responses.

The comparative evidence suggests that European oil majors (BP, Shell, TotalEnergies) are adopting more aggressive decarbonization strategies driven by ESG-conscious investors, stringent EU policies, and social legitimacy pressures, while U.S. majors (ExxonMobil, Chevron) exhibit slower adaptation rates consistent with different regulatory and market contexts.

2.6 Challenges and Opportunities in Renewable Energy Transformation

The transformation from a fossil-fuel-based energy system to a renewable-dominated one represents both a strategic necessity and a complex challenge for global oil majors. The transition is not merely a shift in technology; it is an institutional, financial, and cultural evolution that redefines how corporations operate, compete, and create value. For companies like BP, Shell, TotalEnergies, and ExxonMobil, the move toward renewables entails navigating profound paradigm shifts from resource extraction to knowledge creation, from carbon intensity to sustainability leadership, and from geopolitical dominance to collaborative ecosystems.

While the global energy transition is often portrayed as a linear pathway toward sustainability, in reality it unfolds as a non-linear, multi-dimensional transformation characterized by uncertainty, trade-offs, and systemic interdependencies (Geels, 2014). Oil majors face the dual imperative of maintaining financial performance and energy security while decarbonizing their portfolios. The complexity lies in balancing short-term shareholder demands with long-term societal expectations, making this one of the most intricate corporate transformations in modern economic history.

2.6.1 Financial and Investment Challenges:

The first and perhaps most significant barrier to renewable transformation lies in financial restructuring and capital reallocation. For over a century, oil majors have thrived on the stability of long-term hydrocarbon cash flows. The renewable energy sector, however, operates under fundamentally different economics—characterized by high upfront capital expenditure, lower margins, and longer payback periods.

For example, BP’s commitment to invest $5 billion annually in low-carbon projects by 2030 contrasts sharply with its historic allocation to oil and gas exploration, which exceeded $15–20 billion annually. This shift requires a delicate balancing act: diverting capital toward renewables without undermining the company’s dividend-paying capacity, which remains a key metric for institutional investors. The discount rate disparity between renewable and fossil investments further complicates valuation, as renewable projects typically yield lower internal rates of return (IRR) over longer timelines (IEA, 2022).

2.6.2 Technological Complexity and Integration Risks:

Technological innovation is central to the renewable transition, yet it introduces its own set of complexities. Renewable technologies such as offshore wind, solar photovoltaics (PV), green hydrogen, and energy storage differ fundamentally from the oil industry’s traditional technological paradigm. While petroleum engineering relies on geology, extraction, and refining, renewable innovation revolves around electronic systems, materials science, digital optimization, and systems integration.

This divergence necessitates cross-disciplinary R&D capabilities that oil majors historically lacked. BP’s partnerships with Lightsource BP (solar) and Equinor (offshore wind) illustrate an adaptive strategy: rather than developing all technologies internally, the firm collaborates with specialized partners to accelerate learning. This approach aligns with the Open Innovation Model (Chesbrough, 2003), which encourages firms to combine internal expertise with external innovation networks.However, integration risks remain substantial. Renewable energy markets are fragmented, rapidly evolving, and characterized by technological uncertainty. Choosing the wrong technology path—such as overinvesting in biofuels before the emergence of cost-effective hydrogen—can result in stranded innovation assets. Moreover, scaling up renewables requires new forms of operational agility, real-time data management, and digital infrastructure, pushing oil majors toward a hybrid technological identity that blends industrial engineering with digital entrepreneurship.

In BP’s case, the company’s digital twin systems and AI-driven predictive maintenance tools represent efforts to fuse data analytics with physical energy infrastructure, fostering operational efficiency in both legacy and renewable assets. However, as Teece (2007) notes, such reconfigurations require not only technical resources but also dynamic managerial capabilities to continually sense and seize emerging opportunities.Moreover, the volatility of commodity prices directly affects available capital for transition. High oil prices (e.g., post-Ukraine war) provide liquidity but reduce the urgency for diversification, whereas price collapses—such as during the COVID-19 pandemic limit investment capacity when it is most needed. This cyclical dependency undermines the consistency of transition financing.

Adding to the challenge is the rise of ESG (Environmental, Social, Governance) investment frameworks, which pressure firms to decarbonize rapidly. While ESG compliance enhances reputation and access to sustainable finance, it also raises investor expectations that may not align with operational realities. BP’s green bond issuances and participation in sustainability-linked loans mark progress, but such instruments still represent a small fraction of the company’s total debt structure.

Thus, the financial challenge of renewable transformation lies not only in funding new technologies but in redefining the financial logic of energy capitalism from extractive profit models to sustainable value creation systems (Elkington, 1997; Porter & Kramer, 2011).

2.6.3 Policy and Regulatory Uncertainty:

The energy transition is deeply intertwined with the policy landscape. National governments, multilateral institutions, and regional blocs like the European Union shape corporate transition strategies through carbon pricing, renewable subsidies, and regulatory mandates. However, policy fragmentation across jurisdictions creates uncertainty that constrains long-term planning.

For example, while the EU’s Green Deal and Carbon Border Adjustment Mechanism (CBAM) provide clear decarbonization pathways, other regions—particularly the United States and parts of Asia exhibit more volatile or inconsistent policy frameworks. This heterogeneity complicates the investment calculus for globally integrated firms like BP and Shell, which operate across more than 70 countries.Moreover, carbon pricing mechanisms vary widely from $90 per ton in Sweden to below $10 in major emerging economies creating distortions that limit global cost parity for renewables. As Sovacool (2016) argues, such asymmetry in climate governance leads to “policy patchworks” that favor incremental adaptation over systemic transformation.

Another regulatory challenge lies in permitting and infrastructure deployment. Renewable projects often face lengthy approval processes, land acquisition disputes, and supply chain dependencies on rare materials. BP’s offshore wind projects in the North Sea, for instance, require coordination across multiple national jurisdictions, each with distinct environmental and maritime regulations.

Hence, policy uncertainty acts as both a driver and constraint of corporate transformation. While supportive policies catalyze innovation and investment, regulatory inconsistency can stall implementation and increase the perceived risk profile of renewable ventures.

2.6.4 Organizational and Cultural Barriers:

Transitioning from an oil-centric business to a renewable energy enterprise entails profound organizational change. The cultural DNA of oil majors built on engineering excellence, risk control, and hierarchical management often clashes with the decentralized, experimental ethos of the renewable sector.

BP’s internal surveys (2021–2023) revealed challenges in fostering a “growth mindset” among employees accustomed to the predictability of hydrocarbon operations. The company’s “Performing While Transforming” initiative seeks to address this by embedding agility and cross-functional collaboration into daily workflows. This aligns with Schein’s (2010) model of organizational culture change, emphasizing that true transformation occurs when shared values, beliefs, and symbols evolve alongside strategy.Additionally, the skills required in renewables data analytics, power systems design, digital marketing—differ markedly from traditional oil sector competencies. This creates talent transition gaps, forcing oil majors to retrain engineers, attract digital talent, and redesign incentive systems. TotalEnergies’ “One Tech” program and Shell’s Energy Transition Academy illustrate industry-wide recognition of the human capital challenge.

However, culture can also be a source of opportunity. Oil majors possess robust safety cultures, technical rigor, and project management expertise, all of which are transferrable to renewables. The key lies in cultural integration rather than displacement—creating hybrid organizational identities that blend traditional discipline with innovation agility.

2.6.5 Supply Chain and Resource Dependencies:

Renewable energy systems, though sustainable in operation, are resource-intensive in production. Technologies such as wind turbines, solar panels, and batteries depend on critical minerals like lithium, cobalt, and rare earth elements. The supply chains for these materials are geopolitically concentrated often in regions with governance or labor challenges, such as the Democratic Republic of Congo or China.This concentration introduces new forms of dependency for oil majors entering the renewable sector. BP’s partnerships with battery and solar manufacturers require navigating complex procurement and sustainability verification processes. Moreover, supply chain volatility exacerbated by trade disputes and COVID-19 disruptions can delay project execution and increase costs.

To mitigate these risks, firms are increasingly adopting circular economy models (Geissdoerfer et al., 2017), promoting material recycling and design optimization. TotalEnergies, for instance, has invested in closed-loop recycling for solar modules, while Shell explores end-of-life reuse for EV batteries. These strategies not only enhance sustainability but also reduce long-term operational risk.

2.6.6 Market and Competitive Opportunities

Despite these challenges, the renewable energy transformation presents vast opportunities for growth, innovation, and legitimacy. The global renewable energy market is projected to exceed $2 trillion by 2030, with solar, wind, and green hydrogen leading investment flows (BloombergNEF, 2023).BP’s ventures into offshore wind in the UK and the U.S., as well as its expansion into electric mobility infrastructure, position the firm to capture early-mover advantages in high-growth segments. Moreover, energy diversification enhances resilience by reducing exposure to oil price volatility and geopolitical disruptions.

The shift also allows companies to redefine their social contract with society. As Porter and Kramer (2011) argue in their concept of shared value, aligning business success with societal benefit can create enduring competitive advantage. For BP, participation in decarbonized urban infrastructure, sustainable aviation fuels, and community-based solar projects not only fulfills ESG obligations but also strengthens stakeholder trust.Additionally, the renewable sector fosters opportunities for digital transformation. Through smart grids, AI-based forecasting, and blockchain-enabled energy trading, oil majors can monetize data and create new business models. This convergence of digitalization and decarbonization marks a defining trend in the next phase of global energy innovation.

3. RESEARCH METHODOLOGY

The methodological foundation of this dissertation is grounded in a pragmatic research philosophy, which combines both positivist and interpretivist elements to capture the multifaceted nature of BP’s energy transition strategy. Pragmatism acknowledges that no single philosophical paradigm can adequately explain complex organizational phenomena such as energy transition, which encompass technical, financial, environmental, and socio-political dimensions.

In the context of this study, positivism underpins the quantitative evaluation of BP’s sustainability performance, financial investments in renewables, and emissions reduction progress using verifiable secondary data sources such as BP’s annual reports and global databases. Conversely, interpretivism supports the qualitative analysis of strategic intent, leadership communication, and corporate culture transformation through document interpretation and thematic review of policy statements, sustainability reports, and CEO communications.

The research approach employed here is both deductive and inductive. The deductive dimension involves applying established theoretical frameworks — such as the Dynamic Capabilities Theory, Triple Bottom Line, and Institutional Theory — to assess BP’s energy transition processes. The inductive component emerges from identifying new insights and patterns within BP’s evolving sustainability strategies, drawn from interpretive content analysis of corporate reports and industry literature. Together, these complementary approaches ensure analytical depth, balance, and theoretical grounding.

3.1 Research Design (Mixed/Qualitative, Secondary Data)

This study adopts a mixed-method research design, integrating both qualitative and quantitative elements, but relying entirely on secondary data sources. The rationale for this choice lies in the dual objective of (1) understanding the strategic and cultural dimensions of BP’s transition qualitatively and (2) evaluating the measurable performance outcomes quantitatively.

- Qualitative Component:The qualitative analysis centers on BP’s strategic communications, sustainability narratives, policy responses, and leadership initiatives. It employs documentary analysis to extract recurring themes related to organizational adaptation, stakeholder engagement, and sustainability innovation. The aim is to interpret how BP articulates, implements, and institutionalizes its carbon neutrality strategy.

- Quantitative Component: The quantitative side uses descriptive and trend analysis of publicly available data, such as emissions reduction, renewable energy investments, research and development (R&D) spending, and production portfolio diversification. These data points are obtained from BP’s official Annual Reports (2015–2024), Sustainability Reports, International Energy Agency (IEA) statistics, and UN Sustainable Development Goals (SDG) progress databases.

By combining these two components, the research achieves methodological triangulation enhancing both the validity and reliability of findings (Creswell & Plano Clark, 2018). The case study strategy further strengthens the design by enabling in-depth exploration of BP’s strategic evolution in the broader context of the global energy transition.The focus on a single case (BP) allows for detailed contextualization, while comparisons with peers such as Shell and Total Energies (drawn from secondary literature) provide a reference point for industry-wide benchmarking. This approach aligns with Yin’s (2014) case study method, which emphasizes the use of multiple data sources to achieve rich, contextual understanding.

3.2 Data Sources

Since the research exclusively employs secondary data, data credibility and authenticity are paramount. All data have been obtained from publicly verifiable, reputable sources, ensuring transparency and accuracy. The following are the principal categories of secondary data used:

- Corporate and Financial Reports:

- BP Annual Reports (2015–2024) for financial performance, R&D expenditure, and asset diversification.

- BP Sustainability and Energy Transition Reports for details on carbon emissions, renewable energy production, and ESG metrics.

- Investor presentations and press releases for strategic insights.

- Industry and Regulatory Databases:

- International Energy Agency (IEA) datasets for global and regional energy consumption trends.

- UN SDG and UNEP databases for sustainability indicators and national decarbonization targets.

- OECD and World Bank datasets for energy investment trends and carbon pricing data.

- Academic and Professional Literature:

- Peer-reviewed journals such as Energy Policy, Journal of Cleaner Production, and Business Strategy and the Environment.

- Reports by consulting firms and NGOs (e.g., McKinsey, PwC, Carbon Tracker) providing contextual analysis of the energy transition.

- Comparative Company Reports:

- Annual and sustainability reports of Shell, TotalEnergies, and ExxonMobil, used for benchmarking BP’s strategy against industry peers.

The combination of these diverse sources ensures comprehensive coverage of both macro-level industry trends and micro-level corporate practices, thereby supporting a multi-dimensional understanding of BP’s transition journey.

3.3 Data Collection and Analysis Techniques:

The research employs two main analytical techniques: thematic content analysis for qualitative data and descriptive statistical analysis for quantitative data.

(a) Thematic Content Analysis: The qualitative data (reports, policies, statements) are coded and categorized using NVivo-style analytical logic, focusing on recurrent themes such as:

- Strategic vision and rebranding (“Reimagining Energy”)

- Leadership discourse on carbon neutrality

- Investment narratives in renewable energy

- Organizational restructuring and cultural adaptation

The thematic coding process followed three stages (Braun & Clarke, 2006):

- Familiarization with textual data (reading corporate narratives);

- Generation of initial codes based on sustainability and transition keywords;

- Identification and interpretation of broader themes (e.g., innovation, adaptation, partnership).

This approach allows for identifying how BP’s discourse and actions align with sustainability frameworks and whether there are discrepancies between rhetoric and measurable performance.

(b) Quantitative Descriptive Analysis:

Quantitative data derived from financial and environmental reports are analyzed using trend and ratio analysis. Metrics include:

- Annual R&D expenditure as a percentage of total revenue

- Renewable energy generation capacity (GW) over time

- Carbon emissions reduction trajectory (CO₂ equivalent)

- Return on investment (ROI) in clean energy assets

Descriptive statistics are used to visualize BP’s performance trajectory and to evaluate the degree of progress toward stated carbon neutrality goals. The analysis focuses on pattern recognition rather than causal inference, consistent with the exploratory nature of the study.

This dual analysis (qualitative + quantitative) enables triangulation: qualitative findings explain the why and how, while quantitative data confirm the extent and direction of BP’s transformation.

3.4 Reliability, Validity, and Ethical Considerations:

Ensuring reliability and validity is essential for any research based on secondary data. Reliability refers to the consistency of data interpretation, while validity concerns the accuracy and relevance of data for answering the research questions.

- Reliability Measures:

- All quantitative data are extracted from verifiable public records (BP, IEA, UN), ensuring temporal consistency.

- Qualitative interpretations are cross-checked against multiple independent reports to minimize subjectivity.

- Consistent coding criteria were applied across all textual sources.

- Validity Measures:

- The data sources are triangulated from corporate, institutional, and academic origins to enhance construct validity.

- The conceptual framework (Chapter 2) directly guides the data analysis, ensuring alignment between theory and evidence.

- Peer-reviewed literature and industry verification strengthen external validity.

- Ethical Considerations:

- All data used are publicly available; therefore, no participant consent or personal data processing was required.

- The research adheres to GDPR and academic ethical standards, ensuring respect for data integrity, citation, and intellectual property.

- The analysis remains objective, acknowledging both BP’s progress and its limitations in sustainability claims.

By maintaining transparency, neutrality, and rigor throughout the data handling and analysis process, the study upholds the ethical principles expected of doctoral-level research.

4. COMPANY OVERVIEW-BP PLC

BP plc (formerly British Petroleum) is one of the world’s largest integrated energy companies, with a legacy that spans over a century. Founded in 1908 as the Anglo-Persian Oil Company (APOC) after the discovery of oil in Masjed Soleyman, Iran, BP’s history is intertwined with the development of the global petroleum industry. Initially backed by the British government, APOC was a strategic asset in securing the empire’s energy independence during the early 20th century.

In 1954, the company rebranded as the British Petroleum Company, signaling its evolution from a regional oil enterprise into a global energy corporation. During the post-war period, BP expanded rapidly across the Middle East, Africa, and the North Sea, building one of the most comprehensive oil exploration and refining networks in the world. The discovery of North Sea oil in the 1970s provided a new growth engine, ensuring energy security for the United Kingdom and positioning BP as a cornerstone of the Western oil economy.

The late 20th century marked a phase of consolidation and globalization for BP. The company’s mergers with Amoco (1998), ARCO (2000), and Burmah Castrol (2000) transformed it into a supermajor, allowing BP to strengthen its presence in the United States and diversify its portfolio across upstream, downstream, and petrochemicals. However, these expansions also introduced complexity and operational risk, which would later surface in catastrophic form.The Deepwater Horizon disaster in April 2010 was a watershed moment in BP’s corporate history. The explosion of the Macondo well in the Gulf of Mexico caused one of the worst environmental disasters in history, leading to 11 deaths, widespread ecological damage, and estimated financial liabilities exceeding USD 65 billion. The incident deeply tarnished BP’s reputation and forced a comprehensive restructuring of its safety protocols, governance, and risk management frameworks.

In the post-2010 era, BP underwent a strategic reinvention, aiming to restore trust, stabilize financial performance, and redefine its corporate purpose. Under successive leadership transitions, culminating in Bernard Looney’s appointment as CEO in 2020, BP declared its ambition to become a “net-zero company by 2050 or sooner.” This transformation marks a decisive shift from BP’s historic identity as an oil and gas major to its emerging role as an integrated energy company focused on renewables, electrification, and decarbonization technologies.Thus, BP’s evolution reflects both the opportunities and contradictions of the energy industry a company born in the fossil fuel era now positioning itself at the forefront of the clean energy transition.

4.1 Global Operations and Business Divisions

BP’s operational model is structured around three core business segments, each contributing to its transformation into a diversified energy enterprise:

- Production & Operations (Upstream): This segment encompasses the exploration, development, and production of oil and natural gas. BP’s upstream operations span major geographies including the North Sea, Gulf of Mexico, the Middle East, and West Africa. In recent years, BP has divested several legacy assets and redirected capital toward low-carbon ventures and natural gas, viewed as a transitional fuel supporting the decarbonization of power systems.

BP’s upstream strategy today emphasizes capital discipline, digital optimization (via advanced reservoir modeling and AI-driven analytics), and partnerships that enhance operational safety and carbon efficiency. - Customers & Products (Downstream): This division includes refining, marketing, trading, and distribution of petroleum and bioenergy products. BP operates a global network of refineries, retail fuel stations, and Castrol-branded lubricants. The company is increasingly integrating EV charging infrastructure (through its subsidiary bp pulse) and biofuels as part of its customer-focused decarbonization strategy.The downstream business plays a dual role — maintaining short-term profitability while serving as a platform for long-term energy transformation through mobility solutions, digital platforms, and low-carbon fuels.

- Gas & Low Carbon Energy (GLCE): Established as part of BP’s reorganization in 2020, this division represents the company’s commitment to the energy transition. GLCE focuses on renewable energy generation (wind, solar, hydrogen), carbon capture and storage (CCS), and power trading. BP has invested in global renewable projects such as the Lightsource bp solar joint venture, offshore wind farms in the United States and UK, and emerging green hydrogen projects in Australia and Europe.This business division is projected to be BP’s primary growth engine beyond 2030.